The Maryland HomeCredit Program offering Mortgage Credit Certificates (MCCs) is now closed for new reservations. We do not plan to re-open the program in the immediate future. We will continue to re-issue existing MCCs in the case of refinance; talk to an approved MCC lender for this (see the

full list of MCC lenders).

Mortgage Credit Certificates: The Basics

Eligible Maryland homebuyers can receive a mortgage credit certificate through the Maryland HomeCredit Program, offered by Maryland’s Department of Housing and Community Development.

A "Maryland HomeCredit” allows a homeowner to claim an annual federal tax credit equivalent to 25% of their mortgage interest payments in a given tax year. This can potentially save a homebuyer tens of thousands of dollars over the life of a loan, and makes owning a home more affordable. Together with a home loan through the Department’s Maryland Mortgage Program, which offers Down Payment Assistance and the certainty of a 30-year fixed interest rate, the State of Maryland is making the dream of sustainable homeownership a reality for more Marylanders.

Who Can Get a Maryland HomeCredit?

To get a HomeCredit, a& borrower must be purchasing a home in Maryland and meet borrowing criteria that include:

- The borrower cannot have owned a home during the past three (3) years, UNLESS: 1) purchasing in a

Targeted Area; OR 2) using a veteran's one-time exemption

- The borrower must meet the same

income limits and home purchase price limits as the Maryland Mortgage Program;

- The home purchased must be the borrower's primary residence.

NOTE - the Maryland HomeCredit Program is not available with all MMP loans. Check the product

fact sheets for availability information.

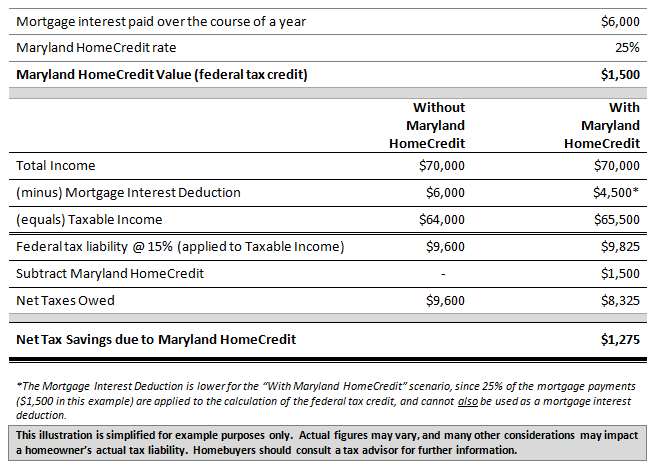

Calculating the Value of an Maryland HomeCredit

The size of the tax credit received by a homeowner with a HomeCredit is 25% of that year's mortgage interest payments, up to a maximum credit of $2,000 in any single year.

Note that the actual net savings due to the HomeCredit are likely to be less than the face value of the tax credit, since the value of the of interest payments associated with the tax credit (25% of total interest payments) cannot

also be used as a standard mortgage interest deduction.

The following example shows a typical calculation:

Our

downloadable calculator can help you estimate how a Maryland HomeCredit can provide you with a borrower with savings over the life of a loan.

downloadable calculator can help you estimate how a Maryland HomeCredit can provide you with a borrower with savings over the life of a loan.

Maryland HomeCredit Fees

Borrowers must pay certain fees to receive a Maryland HomeCredit. Fees for processing Maryland HomeCredit applications may be charged in accordance with HomeCredit Directives, located on the

Directives page.

Refer to the lender's

Compliance Manual for more details.

Compliance Manual for more details.

Lender Reporting Requirements

Any Lender that makes a mortgage loan in conjunction with the Maryland HomeCredit Program and provides a certified indebtedness amount must submit IRS Form 8329, annually, on or before January 31 of the year following the calendar year to which the report relates.

A separate Form 8329 shall be filed for each issue of a HomeCredit associated with a mortgage loan made during the preceding calendar year.

A copy of Form 8329 must be submitted to the Maryland Department of Housing and Community Development's Community Development Administration.

Failure to File

Failure to file the Form 8329 could result in penalties imposed by the IRS.

For more details on reporting, please refer to the lender's

Compliance Manual.

Become a Maryland HomeCredit Lender

Lenders that wish to offer the Maryland HomeCredit Program to borrowers must be approved by the Department's Community Development Administration - Maryland's housing finance agency. See our

Application Instructions.